[Saturday, November 29, 2008

|

]

Time is really bad for KepCorp.

Property division (Kepland & KepBay Reflection) is heading into property grand sales next years.

Infrastructure division has a badly injured victim, Kep T&T falling from sky (>$5) to hell (<$1) in just a month times. Reit division (K-Reit) is presenting unbelievable super yield of 15%.

SPC just reported a 99 per cent fall in quarterly net profit. (Not One 99 shop, ok?!)

Of course, the newest and heaviest blow is reserved to Kep O&M: TALK.

KEP O&M is by far the biggest asset own by KepCorp. The ‘talk’ to arrive at mutually acceptable contract arrangement is bad but not the worst.

In more optimistic perspective, the ‘talk’ may not end in simple cancellation. The current total order book of $12.5 billion shall be enough to safe KepCorp until 2012 when global credit crunch subdued.

KepCorp is hovering 10% dividend yield on last Friday closing. Good buy or good bye? I choose the former.

Continue to read more...

[Saturday, November 29, 2008

|

]

YOU never know when a market hits bottom until well after the fact, but there have been a series of hints over the past few weeks that stock market investors may be flirting with one.

For one thing, volatility is easing. The Chicago Board Options Exchange Volatility Index , or VIX, is down about 8 per cent for the month and around 38 per cent below its 2008 peak hit last month.

A series of sentiment and flow indicators have also suggested this month that, while major investors remain very gloomy about the world around them, they are not getting much gloomier. On Thursday, Reuters asset allocation polls showed that, though leading investment houses continued to hold minimal levels of stocks in their portfolios, they had not reduced exposure this month.

The polls of 45 firms across the world showed equities rose a statistically insignificant 0.1 per cent month-on-month in an average balanced portfolio. Allocations were still well below the roughly 60 per cent long-term average for stocks, but they had levelled. This picture of gloomy- but-not-gloomier investors also emerged from other monthly surveys. State Street's investor confidence index for the month hit its lowest level in its more than 10-year history. But the month-on-month decline was a fraction of what was seen the previous month.

The custodian bank, which compiles its index from the buying and selling patterns of its clients, said that institutional investors were not reacting as strongly to deteriorating economic fundamentals as they had been.

'This month's readings provide a measure of relief,' index co-developer Ken Froot said.

Also gloomy, but with the odd shaft of light, was Merrill Lynch's monthly poll of some 180 fund managers across the world, released last Wednesday.

Although the poll showed investors currently believe the global economy is in recession and it is not going to come out of it for some time, there were signs of asset allocation shifts reflecting stronger risk appetite.

The percentage of fund managers who underweight equities dropped to 54 per cent from 62 per cent, for example, and a run on emerging market equities appeared to have levelled off with 30 per cent underweight versus 36 a month earlier.

Overall, Merrill's risk and liquidity indicator, drawn from the poll's findings, improved slightly. All this may be small beer, but it fits with an increasing number of investors who are arguing that, after falls of more than 50 per cent on many stock markets over the past 18 months, there are bargains out there.

Fortis Investments said this week that one of its tactical funds was moving back into equities and high-yield bonds in part because of value.

Templeton Asset Management's emerging markets funds are betting on a market recovery early next year, with MSCI's benchmark emerging market equity index having lost almost 60 per cent this year.

'Emerging markets have gone very far down and are now back to levels we saw in 2003. We think all these (government stimulus) programmes will start to have an impact in the early part of next year and then we will see a rebound,' said emerging markets guru and Templeton executive chairman Mark Mobius.

This siren song has been heard before, of course, and there is nothing to say that the signs of a levelling off and even renewed investor appetite will automatically lead to an eventual bounce in equities.

The bear market that began last year has already had a number of bounces, including a more than 20 per cent rise between the end of October and beginning of November for the MSCI all-country world stock index .

As analysts point out, bottoming out after steep market falls is a process rather than a specific event. Although in retrospect a bottom price can be identified, it tends not to be spotted at the time. From a process standpoint, the bottom of the last bear market, in 2002-3, came over a roughly five-month period. -- Reuters

Continue to read more...

[Friday, November 28, 2008

|

]

WHILE most Singapore property developers are afflicted by the same predicament - over-supply, low confidence - the Chinese property market is as varied as its landscape.

Take property S-chip CentraLand for example.

Listed here in February, the price of Centra- Land shares at IPO is likely to have priced-in various poor economic data at the time. Even so, its IPO offer price of 50 cents has fallen only 4 per cent since, while share prices of most Singapore-based property developers are more likely to have fallen upwards of 60 per cent.

For the third quarter of 2008, revenue amounted to about 277.4 million yuan (S$62.1 million), recognised from delivery to buyers of 997 units of pre-sold retail and office units in its commercial property project, J-Expo in Zhengzhou.

Located in the Henan province, J-Expo is a wholesale commodities building in the heart of Zhengzhou city, located at the junction of the main road and rail network in central China. In a filing with SGX, CentraLand said Zhengzhou city enjoys good traffic and is an important wholesale centre, especially for women's apparel.

Not many would know this about Zhengzhou, much less know where it is. This being so, CentraLand, which is probably considered more 'exotic' compared to other China property S-chips, is not heavily traded.

Less exotic property S-chips like Yanlord, China New Town Development (CNTD) and Sunshine Holdings are traded more heavily. Their share prices have also fallen dramatically, in line with market movements.

Indeed, since the start of the year, Yanlord, CNTD and Sunshine share prices have fallen 80 per cent, 95 per cent and 92 per cent respectively to very low penny values.

But the paradox is that unlike Singapore (and much of the world) some markets in China, where some of these S-chips have projects, are actually seeing property prices recovering.

Citigroup analysts visiting numerous cities made several conclusions recently. They noted that inner cities like Chongqing and Chengdu looked less affected by the export slowdown and global financial crisis, as their economies are more domestic trade oriented.

In Chengdu, Citigroup added that activity has recovered slightly from the period immediately after the earthquake, but more importantly, it also sees a meaningful difference in terms of sales volume and prices versus the period before the earthquake.

Citigroup did not, however, notice meaningful rebounds in transaction prices and volumes in Shenzhen or Guangzhou, 'and the market is still clouded with the wait-and-see attitude of the potential buyers'.

Citigroup said that in Hangzhou, the provincial capital of Zhejiang province, the situation has been deteriorating, adding: 'As one of China's main export and manufacturing driven provinces, Zhejiang has been significantly impacted by the export slowdown and global financial crisis.'

On the other hand, Citigroup considers Shanghai as one of the most resilient in China, especially for projects located in prime locations. 'We don't see any significant price cuts in the high-end/luxury-end residential projects,' it said, adding that in the past two years, there has also been limited new land supplies in the city centre.

Different Chinese cities also appear to have different property cycles. DTZ Research reveals that property prices in Shanghai peaked at the end of 2005 and then plummeted for a year before rising steadily since the end of 2006.

DTZ's Shanghai property price index rose 40 per cent in Q3 2008 compared with the previous trough in Q4 2006. Prices continued to increased by 3 per cent quarter-on-quarter in Q3 2008 and 5.2 per cent compared with Q4 2007.

In Guangzhou and Shenzhen, however, property prices only peaked in Q4 and Q3 of 2007 respectively. While prices have recovered somewhat in Guangzhou - with the DTZ price index rising 2 per cent since the previous trough - Shenzhen prices have fallen 16 per cent since Q3 2007.

More interestingly, Beijing prices have been increasing for four years, registering an 8.1 per cent quarter-on-quarter increase in Q3 2008.

Each city appears to react to different micro-economic factors like land scarcity, high levels of speculation, or even the efficiency of local governments to implement policy changes (curiously, the Chinese government's relaxation on mortgage lending in October has not had an impact on share prices).

As such, finding value in the Chinese property market takes a lot of work. But at the same time, it should help to separate the wheat from the chaff.

Continue to read more...

[Friday, November 28, 2008

|

]

The latest earnings season has been a chilly one for real estate investment trusts (Reits) hit by the credit crunch and a cooling property market.

Many Reits are working to shore up confidence in their credit positions. Property acquisitions are virtually off the table while industry watchers are divided on whether consolidation within the sector is on the cards.

'Reits are definitely paying more attention to financing,' said DMG & Partners Securities analyst Brandon Lee. The research house estimates that the sector has at least $4.5 billion up for refinancing in 2009 alone. With credit tightening and spreads widening, the market is watching closely for signs of trouble.

According to a CIMB-GK report, borrowing spreads for Reits have risen from an average of 150 basis points (bps) to 200-300 bps for three-year loans in the last six months.

'While average all-in cost of debt for most Reits has been contained within 4 per cent thus far . . . we expect the all-in cost for those with significant refinancing due in 2009 to rise,' said associate vice-president of research Janice Ding.

Reits have tried to soothe market anxiety in the past few weeks by releasing more details on debt. Ascendas Reit (A-Reit), for instance, won confidence votes when it said it had secured firm commitment of $200 million to help refinance a $300 million loan due in August next year.

Suntec Reit also made it a priority to refinance a $700 million loan due in December 2009. 'Whilst we have no major financing needs in the next 12 months, we are keenly aware of the liquidity crunch,' said the Reit manager's CEO Yeo See Kiat last month.

Reits also have to worry about asset devaluation as the slowing economy weighs down on rents and occupancies. Lower property values would raise gearing ratios. Frasers Commercial Trust (FCOT) booked a revaluation loss of $83.5 million in the third quarter ended Sept 30.

Reits have pushed asset acquisition plans to the bottom of the agenda. Even organic growth has slowed. Suntec Reit shelved redevelopment plans for Park Mall. CapitaMall Trust also held back enhancement plans for three malls because of high construction costs.

'We will review new commitments carefully and will not sacrifice our liquidity,' said the Reit manager's chairman Hsuan Owyang last month.

Analysts advise investors to be selective. While low unit prices have boosted yields, it would help to 'pay extra attention to (Reits') refinancing profile, especially the quantum of short-term debt due within the next six to nine months,' said DMG's Mr Lee in a note. 'We like S-Reits with strong sponsors (and) excellent track record.'

CIMB-GK's Ms Ding added: 'The presence of strong sponsors and government-linked sponsors is advantageous at this juncture.'

FCOT, for instance, managed to take a $70 million loan from parent company Fraser and Neave last week to repay debt. The trust is in talks to refinance the $70 million loan and all debt maturing next year. In response, Standard & Poor's Ratings Services took FCOT off 'CreditWatch' status and said that the outlook is stable.

ARA Asset Management Group CEO John Lim believes that consolidation in the sector seems unlikely because Reits would be more concerned about their own refinancing and asset valuation issues.

CIMB-GK's Ms Ding said that in today's market, it would be difficult 'for any single entity to have enough funds to buy over the entire (Reit) unless it's a distressed sale'.

But an industry observer believes that consolidation could happen because the sinking tide has left some Reits looking weaker than their peers. To avoid coughing up cash, a potential acquirer can offer units in itself to the target Reit, he added.

Continue to read more...

[Wednesday, November 26, 2008

|

]

I am very surprise to see a High Note 5 related advertisement on my weblog.

As the advertisement read: Were you misled about the safety of your investment? Contact us.

Someone is coming out with cost to advertise on Adsense now. The exercise may gain more momentum soon with the victims started to group.

Continue to read more...

[Tuesday, November 25, 2008

|

]

The Minibond saga is still hot and Hong Lim is still crowded. Part of the issues is allegation of misrepresentation and mis-selling by below qualified banking personnel to unsuitable group of customers.

I am not surprise to read in Singapore Salary Handbook by Kelly Services the following:

The text:

Position: Bank Teller

Job Description:

Handle high volume of over-the-counter transactions. Assist with customer enquiries, ensure service delivery standards are met & actively promote bank products and services.

The products and services could include Minibond? ILP? Endowment Plan? Insurance?

Guess what is the qualification required for them to discharge the duty to ACTIVELY PROMOTE BANK PRODUCTS AND SERVICES?

‘N’ levels with CO S / ’O’ levels

Maximum salary is $1,900

Continue to read more...

[Tuesday, November 25, 2008

|

]

If you want to know how tough is the current IPO market, look no further then Singapore market.

We have not seen any new IPO for about 2 months since the last. Whereas last year we may have 2 or even 3 IPOs running concurrently.

The latest IPO on hand is Otto Marine launches IPO at 51 cents apiece. They are an offshore marine group engaged in shipbuilding, ship repair and conversion and ship chartering.

If they launch their IPO one year ago, their share will be selling like hot cake, but no now. Instead, no one will bother to write a letter to newspaper forum to complaint that there are only 1 million shares for public offer out of total 235.3 million.

The application period is short, just 4 days.

My perception is that they do not even bother about the public response. The issuer probably has factored in lukewarm response.

Now, look at the history.

In last IPO, China Kunda has launched at 21.5 cent apiece and maintained the share price above water consistently throughout the most volatile month in near term history. China Kunda last traded at 24 cents now. Impressive despite the lack of liquidity (but with close spread).

The possibilities of share price ‘intervention’ by interested parties are high. The chance that Otto Marine to repeat the performance of China Kunda is relatively high.

Continue to read more...

[Tuesday, November 25, 2008

|

]

The research report from DMG Research is very interesting in providing an overall outlook of STI in coming months.

The research report from DMG Research is very interesting in providing an overall outlook of STI in coming months.

STI closed at 1620 points yesterday and today may bounce up to test 1700 points resistance due to strong gain in U.S. market overnight.

For STI to hit 1391 points on January 2009, a further cut of 300 points in December 2008 alone is required. This represent a potential plunge of 17%.

Not impossible. We probably have to postpone the Christmas shopping spree to Chinese New Year!

Continue to read more...

[Tuesday, November 25, 2008

|

]

The title is from breakingviews.com and I think the editor is humorous to link the latest development with Citi famous advertisement slogan.

The title is from breakingviews.com and I think the editor is humorous to link the latest development with Citi famous advertisement slogan.

Citi is paying 8 per cent dividend on US$20b of capital the U.S. government injected in the form of preferred shares. The housing loan board rate is about 4% in Singapore. How do they make profit from -4% gross returns from every loan dished out?

My formula is likely inaccurate, but, the cost of doing business by Citi is definately increasing.

The editor is quick to highlight that it isn't absolutely clear that Citi is out of the woods. As AIG has to come back for second time for rescue package, Citi may repeat it also.

As highlighted, the rescue doesn't address the diffuse concerns that the bank is either unmanageable or badly managed.

Continue to read more...

[Monday, November 24, 2008

|

]

The U.S. government agreed Sunday night to rescue Citigroup Inc. with a plan that includes a $20 billion capital infusion and guarantees for up to $300 billion of Citi's troubled assets, according to media reports.

By MarketWatch

Last update: 12:34 a.m. EST Nov. 24, 2008

http://www.marketwatch.com/news/story/Citi-US-bailout-talks-reports/story.aspx?guid=%7B15A026EC%2DCEA0%2D4C82%2D92EC%2D199B794F0968%7D

Continue to read more...

[Monday, November 24, 2008

|

]

If you still wondering why a rally of close to 500 points last Friday at Dow Jones has no impact to Asia markets, then you have not read/hear/watch any printed media/radio/TV this morning.

Here is three lines for you from ST today:

Any Asian rally today likely to be short-lived with sentiment still fragile amid tensions

Regional markets will enjoy an obligatory knee-jerk rise today and give them another opportunity to get rid of their stocks at a higher price.

Few traders expect the stock market rally to have legs.

Continue to read more...

[Monday, November 24, 2008

|

]

[Saturday, November 22, 2008

|

]

Sad to say, but have to admit that in last one year, yield-play stock is one of the most poisonous and dangerous investment.

Sad to say, but have to admit that in last one year, yield-play stock is one of the most poisonous and dangerous investment.

The market is volatile and spiral downward for the last one year. Even though there is no one sector being spare in this downturn, however, the temptation of high dividend yield has attract sizeable group of passive investor to join the massacre.

This is very true to REIT and shipping trusts in Singapore.

The minibond investors have risked full invested amount for potential 5% return.

The REIT and business trust is looking at the potential payout of 30.8% (MI-REIT) and 45% (FSL Trust) among the highest.

If the return is commeasurable with the risk, and vice versa, then, we may be waiting for another round of saga.

Continue to read more...

[Saturday, November 22, 2008

|

]

WHEN there is extreme uncertainty and volatility in financial markets, investors become unsure about where to park their funds. So holding cash may seem the safest option. But is cash really as safe an option as it seems - even now when a global recession is looming and asset prices are falling? The answer depends, among other things, on your risk appetite and investment horizon.

Before we delve into the topic, it is important to highlight that holding cash is not a risk-free option, especially when inflation runs ahead of interest rates.

In Singapore, for example, the annualised inflation rate in September was 6.7 per cent - substantially higher than fixed- deposit rates, which range from less than 0.5 per cent to less than 2 per cent, depending on the tenor.

Even at next year's officially projected inflation rate of 2.5 to 3.5 per cent, real interest rates - that is, the difference between deposit rates and the inflation rate - would still be negative. So those holding cash will still suffer wealth erosion.

So are you be better off investing your cash, given that equity markets seem more attractive after the recent huge correction? Our take is that investors should not let their guard down just yet - the outlook is still fraught with uncertainty.

Obviously, equity markets have come off very sharply. The MSCI World Index, for example, has sunk more than 40 per cent this year. In Asia, the correction in some markets has been even more pronounced, with bourses like China having declined more 60 per cent this year.

The sell-off has made markets less pricey, with forward price/earnings multiples now in the low teens or even at single-digit levels. Consequently, investors may find it tempting to go head-long into equities. However, this may not be the best strategy - and there are good reasons to stay cautious right now.

True, fears of the global banking system collapsing have eased and credit markets have shown signs of improvement. However, the situation is far from normal and it could take several months if not years before 'order' is restored.

Banks will need time to recover substantial losses and recapitalise their balance sheets. Hence, they are likely to stay cautious and may not resume normal lending any time soon.

We are already starting to see signs of forced selling and de-leveraging in the US$2 trillion global hedge fund industry. As funds' returns suffer, investors are pulling out money, while banks and prime brokers are cutting their leverage and demanding more collateral. As a result, hedge funds are forced to sell off assets to cover redemptions and meet margin calls.

In the US, the housing slump is hardly over. Home prices there are still falling and the rate of mortgage foreclosure is expected to rise in the coming months, especially when adjustable-rate mortgages are reset. Over the next two years, ratings agency Fitch has estimated that a sizeable US$96 billion of adjustable-rate mortgages will be reset higher.

Companies will also continue to unwind their debt holdings and investments, bought with the help of borrowed money, which will further drag down the market prices of many assets, including equities, causing yet more losses for investors.

Even if the central bank rescue efforts help calm conditions in credit markets and the nerves of jittery investors, this may not be enough to prevent a drawn-out global recession. Also, the write-downs may not be over. Global financial institutions may need to make more provisions as the value of assets on their balance sheets could diminish further and losses will be realised if these assets are sold at current market value. Given the risk of a deep and protracted recession, corporate earnings forecasts for next year, which appear to be too optimistic, may miss the mark in coming quarters, and this is another factor that could weigh on equity markets as profit estimates are cut. Given the risk of further downside, those who are looking to bargain-hunt at this time must have a strong risk appetite and a long-term investment horizon, as equity markets are likely to remain volatile and full recovery may not take place for several months at least.

Anyone looking to buy now should also spread their investments out over the next few months, instead of trying to time the markets. Time diversification aside, investors should also stay diversified across asset classes to protect against downside. It is especially important at this time not to get carried away with specific themes - no matter how appealing they may seem - and over-invest in them.

Despite the current turbulence, equities are still a good long-term bet and markets in Asia and emerging regions should resume their uptrend once the dust settles. However, this does not mean you should plough all your investments into equities. Instead, work out a suitable asset allocation strategy based on your risk appetite and long-term goals. If you're not sure how to do this, seek the help of a qualified financial adviser.

Staying largely in cash for now may seem like a good option if you are convinced that markets have not bottomed. But buying at the bottom is also near to impossible - so if you are afraid of missing the boat, then go ahead and nibble.

Investments are necessary to grow your wealth. Staying in cash for too long is clearly not a long-term option, because the negative real return will erode your wealth and leave you worse off in your golden years. Investments are still a good way to growing your wealth and the current turmoil in markets will throw up attractive opportunities for those with the risk appetite and the foresight to look beyond the current crisis.

Vasu Menon is vice-president, group wealth management, OCBC Bank

Continue to read more...

[Friday, November 21, 2008

|

]

The fact that U.S. stocks have nose-dived into lowest level in more than 11 years is good reason to expect some form of rebound.

It is not likely that U.S. Congress will ignore automakers when they have generously come out with close to trillion dollars to rescue financiers.

The good news now is that: There is no un-known bad news.

The Asian markets have plunged for a ninth straight session and that shall bring out reasonable number of bargain hunters, and, that include MYSELF.

Nonetheless, bottom fishing shall be progressive. Use cash which can be spared for at least 5 years ONLY.

Continue to read more...

[Thursday, November 20, 2008

|

]

Straits Asia, Noble and Olam plunge more than 12%; key commodities index falls sharply

Straits Asia, Noble and Olam plunge more than 12%; key commodities index falls sharply

MAJOR commodity-related stocks here were pummelled for a second day yesterday as investors fretted over slowing economic growth and falling demand worldwide for energy, metals and agricultural resources.

Shares in Straits Asia Resources, which owns two coal mines in Indonesia, plunged 14.5 cents or 19.3 per cent to 60.5 cents, extending its two-day loss to 25.3 per cent.

Chief executive Richard Ong bought one million shares in the open market at an average price of 67.6 cents yesterday, raising his direct stake in the company to 0.592 per cent from 0.501 per cent, according to a Singapore Exchange exchange filing. Straits Asia's shares have slumped 80.6 per cent this year.

Olam International, which supplies agricultural commodities worldwide, saw its shares fall 12.3 per cent to 93 cents, extending its loss since Monday's close to 23.8 per cent. Since the start of the year, its shares have fallen 66.9 per cent.

Shares of Hong Kong-based Noble Group, which manages the global supply chains of various raw materials in food, energy and metals, fell 14.9 per cent to 74 cents, down 23.3 per cent in the past two days. The shares are off 63.5 per cent this year.

In a report yesterday, Credit Suisse analyst Haider Ali cut his target price for Straits Asia to $1.20 from $1.25, while keeping his 'neutral' rating on the stock, citing lower estimates of coal production in the next two years due to a delay at one of its mines.

And earlier this week, Merrill Lynch downgraded its rating on Olam to 'underperform' from 'neutral' and slashed its target price for the stock to $1 from $2.60, after Olam's management said it would cut the proportion of debt on its balance sheet.

This means Olam's aggressive pace of growth in recent years will have to slow, said Merrill Lynch analyst Chong Han Lim. 'By our estimates, the reduced gearing would lower sales-generating potential 30-40 per cent. The revision appears voluntary, but the company is probably making the announcement ahead of the inevitable - bankers tightening lending standards.'

Prices across a broad range of commodities have been hurt badly by a severe deterioration in the global economic outlook, which has triggered fears among investors that the earnings of companies such as Noble and Olam will suffer.

The Reuters/Jefferies CRB index, a global benchmark for commodity prices, fell on Tuesday to its lowest close since Sept 26, 2003. The index, which tracks 19 commodities including aluminium, crude oil, gold and soya beans, has collapsed almost 50 per cent from its all-time peak on July 2 this year, as the financial crisis wreaked havoc on the world's biggest economies.

Physical trade of commodities has also been damaged by the seizing up of credit markets, with firms finding it harder and more expensive to get letters of credit - a common method of payment for goods in international trade - as banks shy away from guaranteeing payments.

International trade is expected to slump 2.5 per cent next year, the first decline since 1982, hurt by shrinking demand and a sharp contraction in trade finance, the World Bank warned last week.

Continue to read more...

[Wednesday, November 19, 2008

|

]

Can't even type the important date probably.......

Quote from the announcement:

The second paragraph of the notice referred to “27 November 2008” which was a typographical error. The date is 28 November 2008, as stated in the separate announcement relating specifically to books closure, also issued yesterday.

http://info.sgx.com/webcoranncatth.nsf/VwAttachments/Att_532C29E5C8C348204825750100232741/$file/081114_Clarification_of_Books_Closure_Date.pdf?openelement

Okay, just rumbling. However, it is really hardly find good reason for today's sell down.

Any?

Continue to read more...

[Wednesday, November 19, 2008

|

]

TANJONG Pagar town council said yesterday that it did not buy any Lehman Brother bonds directly but that one of its fund managers, Lion Global Invest, bought $250,000 of Lehman bonds.

This translates to 0.14 per cent of the council's $179 million sinking fund.

The disclosure comes after Parliament heard on Tuesday that Holland-Bukit Panjang and Pasir Ris-Punggol town councils invested a total of $12 million in DBS High Notes, Lehman Brothers Minibond Notes and Merrill Lynch's Jubilee Series 3.

Six other councils, including Tanjong Pagar, reportedly invested a total of $4 million in Lehman Brothers via portfolios.

Tanjong Pagar town council said yesterday that it is in a strong financial position and takes a prudent approach with council funds. Some 22 per cent of its sinking fund is handled by fund managers, but the bulk of its investments are in fixed deposits and government and statutory board bonds.

Its fund managers were given a mandate to invest over a three-year period, and funds are regularly reviewed by the town council, though the portfolio mix is left to the fund managers' discretion, the town council said.

Continue to read more...

[Tuesday, November 18, 2008

|

]

About 50 homebuyers walked away from deals in October

About 50 homebuyers walked away from deals in October

BizTimes 18 Nov 08

The number of private homes returned to developers shot up last month on the back of a sharp dive in confidence due to the stockmarket crash.

Homebuyers returned 50-odd units to developers in October, compared with 10-plus units each in the preceding month and in October last year. The figures were estimated by BT from statistics on developers' sales released by the Urban Redevelopment Authority (URA) yesterday. The figures exclude executive condos.

October also saw developers launching and selling the lowest number of private homes since URA started making monthly housing sales data available in June last year. Developers sold 112 private homes in October, down about 70 per cent from 376 units in the preceding month and 80 per cent below the 566 units sold in October last year. The 159 private homes developers launched last month was also 79 per cent lower than September and 75 per cent below that in the same year-ago period.

Buyers who returned the 50-plus units last month probably did so before the options were due to be exercised, industry observers reckon. Buyers who walk away from a deal before the option is exercised forfeit a quarter of the 5 per cent option fee, equivalent to 1.25 per cent of the purchase price of the unit.

'The stock market was at its worst in October. So some buyers may have got jittery and decided it was better to forego 1.25 per cent of the purchase price - that's $12,500 for a $1 million property purchase - than to be saddled with uncertainty. They worry that property prices may drop much further in the next six months. So it's a matter of weighing risks, even for people who can afford to take the hit,' said a seasoned property agent.

Another industry observer said another factor for the forfeitures could be if buyers failed to secure the required quantum of housing loan from banks, which have become more cautious in lending. 'Some buyers may also have observed developers trimming prices and got cold feet,' he added.

On a brighter note, he does not expect the number of units returned to developers to keep rising in the months ahead. 'Anybody who buys now must have done his homework. Things are a lot clearer now.'

Agreeing, DTZ executive director Ong Choon Fah said: 'October was an exceptional month with so much stockmarket turmoil and fear all around. Hopefully, we won't get a repeat of this. People will be much more considered when buying homes henceforth and therefore the number of units returned should revert to a more normal situation.'

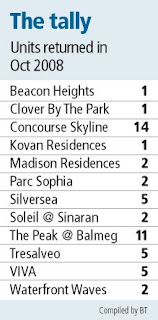

October saw a total of 14 units returned at Concourse Skyline at Beach Road, 11 units at The Peak @ Balmeg in the Pasir Panjang area and five units each at Silversea at Amber Road, Tresalveo at Marymount Terrace and VIVA at Thomson Road/Suffolk Walk. Nonetheless, all these projects still saw units being sold in October.

CB Richard Ellis (CBRE) said, based on transacted prices, prices have 'remained fairly stable for the past two months, with due consideration that factors such as floor height, orientation and liveable space affect prices'.

'However, it is very likely that the persistent thin volume will have a downward effect on prices. The sluggish sales momentum is likely to remain for the rest of the year as macro factors such as the economic recession and retrenchment will erode consumer confidence,' CBRE's executive director Li Hiaw Ho added. He predicts Q4 may see sales volume of around 500 units, a level last seen in Q1 2003.

Knight Frank director Nicholas Mak said that homebuying sentiment is expected to weaken in the face of economic and job market uncertainties. 'Launches are expected to be held back till at least after Chinese New Year 2009,' he added. The lowest-priced apartment/condo sold in October was a unit at The Linear ($554 psf) while the highest-priced unit was an apartment at Orchard Scotts ($2,407 psf).

Savills Singapore's Ku Swee Yong noted that despite a weak month, The Lakeshore in Jurong and Hillvista in the Hillview area crossed $1,000 psf. The $2,169 psf of land area achieved at Sandy Island on Sentosa Cove is probably the highest price for a landed home in Singapore, he added.

Around 63 per cent of the 112 units sold in October were in Outside Central Region. However, in terms of the 159 units launched in the month, the lion's share (46.5 per cent) were in the Core Central Region.

Continue to read more...

[Saturday, November 15, 2008

|

]

The Edge- 16 November 2008

The Edge- 16 November 2008

Property counters were among the first sectors to peak and turn down in June 2007. While few believe that the bear market could possibly have come to an end, some signs are emerging that selected counters could be gaining strength against the sector and the market. Strangely, the stocks are not among the top picks by analysis.

Capitaland was recently downgraded by several analysts, yet the stock is showing signs of superior relative strength. Wheelock Properties is the other counter that has strengthened against the market.

Capitaland – Attempting to bottom

City Development – No change in direction yet

Keppel Land – Still weak

Guocoland – Rate of decline slows

United Overseas Land – Early signs of a base formation

Wheelock Properties – Attempting to form a base

Continue to read more...

[Saturday, November 15, 2008

|

]

US is first world country.

US is first world country.

China is third world country.

US has to spare no effort to approve the $700 Billion bail out plan to restore confidence in the volatile investment market.

However, China has rolled out $586 billion stimulus package like just a small change. China do not need bail out fund too.

The centric of the financial world may be tilting after the crisis.

Let's see.

Continue to read more...

[Saturday, November 15, 2008

|

]

Warren Buffett’s Berkshire Hathaway Inc. fell below $100,000 a share for the first time since 2006, dropping for a fourth straight day after posting a 77% profit decline on Nov. 7.

Berkshire slipped US$6,283, or 6.1%, to US$97,050 at 12:40 p.m. in New York Stock Exchange composite trading. The Omaha, Neb.-based firm’s shares are down about 32% this year.

Berkshire has posted four straight profit declines, the worst streak in at least 13 years, on investment losses and falling returns at insurance businesses.

October’s slump in debt and stock markets reduced the value of Berkshire’s holdings and derivative contracts and caused shareholders’ equity to fall by about $9-billion during the month. “There have been larger declines in the rest of the insurance industry, and Berkshire isn’t immune to that,” said Bill Bergman, an analyst for Morningstar Inc. in Chicago. Bloomberg News

Continue to read more...

[Saturday, November 15, 2008

|

]

Who want to do a year end shopping for half the price condominium? You may do it this weekend in River Valley.

I read with interest the news that the price of condominium is plunging fast and the transaction volume is shrinking. The fact that luxury condominium Luma is going to be relaunched this weekend with about 50% discounts to last year $2,800 psf price tag is shocking.

When the market is red hot last year, the so call market expert is predicting that price is going to go up another thousand dollar psf. This is not dissimilar like analyst predicting that crude oil price will hit $300 per barrel when it hit $140 at peak. Crude oil is selling in less then $60 now.

Who need an expert now?

Continue to read more...

[Wednesday, November 12, 2008

|

]

I am a little surprise with the opinion expressed by a reader’s letter to BT’s Mailbag yesterday: “Don't school kids in personal finance”

Here is the letter (in blue color again) and my personal comment:

I REFER to your editorial, 'Lessons from the Mini-bonds saga' (BT, Oct 30). I have to disagree with your suggestion 'to teach the most important basics of personal finance to our children in school ...'

Me too, but on yours. :-)

My reasons are that first, personal finance is not a subject that can be taught to children in their early teens as it requires a certain level of maturity.

When a person is matured then it will be too late to mould the financial behavior!

Second, a little knowledge may be dangerous.

Yah, but no knowledge is even more disastrous!

And third, it is likely that instead of developing the likes of Warren Buffet, we may end up creating a 'greed is good' mentality.

The objective of personal finance education is not to ‘develop the likes of Warren Buffet’ and it should never be. I did not realize that personal finance education is to instill ‘greed is good’ mentality?!

Therefore, the teaching of personal finance should be deferred until the children reach the tertiary level.

How many of Singaporean never reaches tertiary level? Some not even secondary! Why are they being deprived of personal finance education? Personal finance is affecting the life and living of themselves and their family for whole life!

In the schools, they should be taught fundamental human values which can lead to the building of a caring and sharing society.

We should not just repeating the fairy tales and not explaining to them how their parents able to afford and put food on the table!

Personal finance is not about teaching kids how to trade forex with margin leverage, but can be as simple as instill disciplin to keep extra pocket money into piggy bank.

Please start early!

Continue to read more...

[Wednesday, November 12, 2008

|

]

Here is an interesting comment (in blue) from SGDividends on my previous post Capitaland Shortist Club and I am going to reply here:

Hey dude, do you mean that Capitaland will face download pressure on its price due to the rumour?

Yes! Cash is King and when you decided to distant yourselves from the King during credit crunch time, you will be disliked by the market.

This Sand pie is huge to be swallowed alone or in half. By putting so many eggs into a single basket will definitely attract research houses to downgrade the stock price to reflect higher risk exposure for sure. When property price is poised to slide further next year, the appetite for risk is pretty low.

Even at current stage, the price tag is unlikely to be fire sale price. Simply put it, the seller is not desperate enough with government clear backing now.

Shouldn't it be a good news for Capitaland, just wondering?

Casino is evil good business but not an IR. These IR is generally expected to lose money for a few initial years before they sucked enough winning to pay for the loan interest. If Capitaland use the same quantum of capital to seize up smaller distressed property and development in the region, I believe they will be able to give better return in area they are expert.

The key is: RISK and market don’t like RISK now.

Anyway they recently are looking to divest their industrial property. So rumour might have some truth.....

Divestment of their industrial property is old news. In fact, they have divested retail shopping mall and commercial property into REIT in Singapre and China etc. I don’t think they need to divest these property just to finance their potential bid, anyway. They are big enough to take it, but, at what COST?

Continue to read more...

[Tuesday, November 11, 2008

|

]

If Capitaland is participating in Marina Bay IR, I think we can orgainize a premium "Capitaland Shortist Club" based in Raffles Hotel.

""CapitaLand is trying hard to play down expectations but in the eyes of some analysts, it has emerged as the frontrunner in the race to become Las Vegas Sands' (LVS) white knight. The fact that CapitaLand had participated in the Request for Proposal for both integrated resort (IR) sites here is fanning such talk further.""

--- BT 11 November 2008

Continue to read more...

[Sunday, November 09, 2008

|

]

Golden Agri Resouces – Huge Bargain?!

As tabulated in The Edge this week, Golden Agri has historic price earning ratio (PER) of 0.59 times, well below 1.

As PER is affected by 2 important parameters, there are 2 potential scenarios:

Scenario 1:

The stock price has dropped so low that the earning of Golden Agri in one year time is sufficient to cover not only in full, but exceed all the capital invested now.

Scenario 2:

The earning of the stock is inflated, not sustainable and bound for deep correction.

However, the historical PER shown on Golden Agri home page has given a difference figure: 1.157 times.

As retail investor, I always have a problem to obtain the reliable data from free source when the figure difference in various sources. Nonetheless, Golden Agri seems to be a good bargain either in 0.59 or 1.157 times historical PER.

NAV $0.582 for a stock last traded at $0.205 is like a sexy babe waving at you: Simply tempting but dangerous (for guys, of course :-)).

Anyway, we have the choice.

Continue to read more...

[Saturday, November 08, 2008

|

]

Just want to quote an encouragement type of story (previously published on BT, if I am not wrong) to share with the group of investor who hunting for yield stock:

Altria, formerly Philip Morris, famous for its world's best selling cigarettes brand, Marlboro, was also very well known for its high dividend payments to its shareholders. A sum of US$1,000 placed in Philip Morris back in 1957, with its dividends reinvested, would have grown to almost US$4.6 million today, according to Jeremy Siegel's 2005 book, The Future for Investors.

**(Investsgx: Based on last Friday closing price, Philip Morris is traded at $42.20, with 52-week high $56.26 and 52-week low at $33.30. The range of trading price clearly indicated a classical behavior of blue chip with stable yield in bear market.)**

Investors who reinvest their dividends and accumulate more shares during the bear markets will eventually recoup the price loss because the lower price allows them to own more shares than they would be able to buy if the stock had not declined. Consequently, the value of these extra shares will surpass the magnitude of the stock price declines, making these investors better off overall.

**(Investsgx: Stay tune and cheers!)**

**(Investsgx: http://forum.channelnewsasia.com/viewtopic.php?t=195250

Dividend yield is relevant and will always relevant.

What we need to ascertain is to find out whether the company will be able to sustain its dividend payout over the long term.

Suggest to look at 2 payout ratio:

Payout Ratio of dividends as a percentage of free cash flow

Payout Ratio of dividends as a percentage of net income

The stocks with low payout ratio are more likely to sustain the dividend payout. For stocks which close to 100% or even more then that, we shall avoid it.

)**

Continue to read more...

[Saturday, November 08, 2008

|

]

More then one month after the list of so call

High Yield stock published in the Edge, I intend to do a review of the performance on it this weekend if free, stay tune!

[Thursday, November 06, 2008

|

]

Iceland was once considered one of the developed country before the financial crisis. However, their financial sector has collapsed and its inflation rate is potentially soar to above 20% in 2009.

Their previous unemployment rate is consistently low at about 2.5%, similar to Singapore. However, the unemployment rate is expected to hit 10% very soon.

Singapore has some similarity with the background of Iceland. Let’s wish the policy makers in Singapore learnt a lesson from Iceland failure.

Nonetheless, the public shall be vigilant in monitoring the government strategic. Not to be ignored, the elected President has handed over the key to Government to tap on the reserve to guarantee the deposit in the banks.

Continue to read more...

[Tuesday, November 04, 2008

|

]

This actually is an interesting letter sent to the Editor of Business Times and published on 4 November 2008.

Open Quote:

THE just-announced government's move to suspend the sale of state land for the first half of next year 'was met with jubilation in property circles', reported The Business Times on Nov 1, 2008. The report also quoted a spokesman for City Developments as saying: 'We hope the government will continue to monitor the situation and introduce more pro-active measures to stabilise the property market.'

It is funny to read this because last year, when the Singapore property market 'became 2007's hottest global market with prime capital values increasing by 50 per cent', in six months (source: Jones Lang LaSalle, July 20, 2007), none of the Singapore developers then had urged the government to introduce pro-active measures to stabilise the property market.

The question is: should the government introduce more pro-active measures to stabilise the property market?

I don't think so. If the government is seen to always provide help to developers when their bets go wrong, then developers (and property speculators) will be emboldened to reckless risk-taking behaviour. Property developers and speculators made fantastic profits in good times.

In bad times, they should suffer the consequences of making the wrong bets. Let market forces rule. It is not the government's job to ensure that property developers and speculators come out tops every time. Let the possibility of failure and, real failure, be the necessary market discipline. Genuine buyers of property would be better served this way.

Close Quote

Since the reader posted the question, I would like to express my view too.

First of all, we should not expect any developers to release statement to hit their own toes. Secondly, the government did put up some curb to prevent the property price run away. The termination of deferred payment scheme is a good example. Next in my mind is that the government has raised development charge to slow down en bloc in 2007 too. These measures have successfully prevented the hard landing of property price, at least, up to today.

The second part of the question is: Should the government let the property developers and speculators fail?

The answer is directly link to the principle of free market with or without government intervention. This sound similar to either US government shall rescue the financial institutions or shall let them bankrupt. The academic argument can be very lengthy but without conclusion. In practical, this is not a choice. In the name of national interest, you have to do it and redo it again whenever required.

Continue to read more...

[Monday, November 03, 2008

|

]

COSCO Corp Singapore's Cosco (Zhoushan) Shipyard unit yesterday announced that it is owed US$12.4 million by the owner of three Russian-owned fish processing vessels that it undertook repair works for.

The repairs were carried out from August 2007 to October this year. After completion of the work, a sea trial was carried out on Oct 20. However, the crew unexpectedly changed the vessels' course and did not return to their original point on the following afternoon. To compound the situation, 15 Cosco shipyard workers were on board at the time.

However, with the assistance of the Chinese government, the 15 workers returned safely to Cosco Shipyard yesterday. Only US$3.8 million of the US$16.2 million total contractual price for the repair has been paid.

Cosco Shipyard has demanded payment of the outstanding sum in line with the terms of the contract with the owner of the vessels. It is unclear if Cosco has possession of the vessels.

The outstanding sum is not expected to have a material impact on Cosco's net tangible assets and earnings per share for the year ending Dec 31, 2008, the company said.

Cosco shares closed two cents higher at 77.5 cents last Friday.

Continue to read more...

[Sunday, November 02, 2008

|

]

DBS – Attempting to bottom

Resistance/breakout is at $2.50. Support is at $11

OCBC – Temporary bounce

Breakout level is at $5.35, target $6. Support at $4.80

DBS 6% NCPS 10 – Set to test resistance

Resistance $100, target $107.

Hong Leong Finance – A developing bear flag

Resistance $2.20. Support at $2, target $1

UOB – Trying for a rebound

Resistance/breakout at $13.64. Support at $12.74

OCBC 4.5% NCPS – Excessively oversold

The start of the gap at $76 provide resistance.

Continue to read more...

[Saturday, November 01, 2008

|

]

When US stock index futures getting less reliable, it getting more popular locally as predictors of market movement in pre-market. A lot of people trade by looking at it, and just to reliase that the trend reversed after the close of local market.

Recently there are an article in Bloomberg offering some insight into it, the following is the excerpt:

US stock index futures are becoming less reliable as predictors of market moves. With trading in US stock index futures running more than 23 hours a day on weekdays, their movement can affect sentiment around the world.

While futures may be becoming a worse predictor amid unprecedented actions by central banks to bail out the financial system, pre-market trading is only an indication of what might happen. They're just people's best idea on the market at a time when there are no actual trades.

There was a sense of panic. In the futures markets there are huge swings ahead of the opening. It looks like a casino for global traders.

Continue to read more...

[Saturday, November 01, 2008

|

]

With every passing week, investors are feeling increasingly encouraged that no new disaster bad news worth worrying them again. The stock market has started to recover this week after Investors are throwing caution to the wind.

I realized that increasingly high number of people searching for high yield defensive stock aka blue chip when the search engine keyword ‘dividend’ hit a new high. I believe these are long term passive investors who intend to bottom fish.

While bottom fishing is thrilling and exciting, bargaining at a valuation even lower then what market guru WB get is even more self-fulfilling, but I still believe Cash Is King at this moment.

The Federal Reserve's 50 basis point interest cut is a clear sign the American economy is in danger of crashing. The measures to counter the financial crisis may or may not work. The risk of down side is still very huge with a pending full recession in 2009.

What’s more? I realized that a lot of people still very cash rich and eager to have a bit of the ‘bargain’ now. This puzzle me as there should be cash strapped, out of job, negative asset, bad credit card loan, default mortgage, pay cut etc in a recession. Apparently the full blow of US sub-prime tsunami has not hit Singapore shoreline yet.

I am not aware of what is the story in today's Edge, however, it is good to highlight the risk for investing in emerging markets when the 'perceived value bargain' flooded the market.

Patient get pay. Bottom fishing, may end up with a snake!

Continue to read more...

{kind=link}